A credit card account tracks what you owe — its balance runs negative as you spend on it and moves back toward zero when you pay the bill. Wealth Mutant models the full card cycle, not just a number.

Setting up a card

When creating the account, alongside the opening balance (what you owed at that moment) you set two days that define your cycle:

- Statement day — the day your bank closes the billing cycle and generates the bill.

- Due day — the day payment for that bill is due.

Spending on the card

Record purchases on the card exactly like any expense — same form, the card as the account. The expense is counted when you swipe, in that month's spending, which is when the decision actually happened. Owing the bank for it is a separate fact the card balance carries.

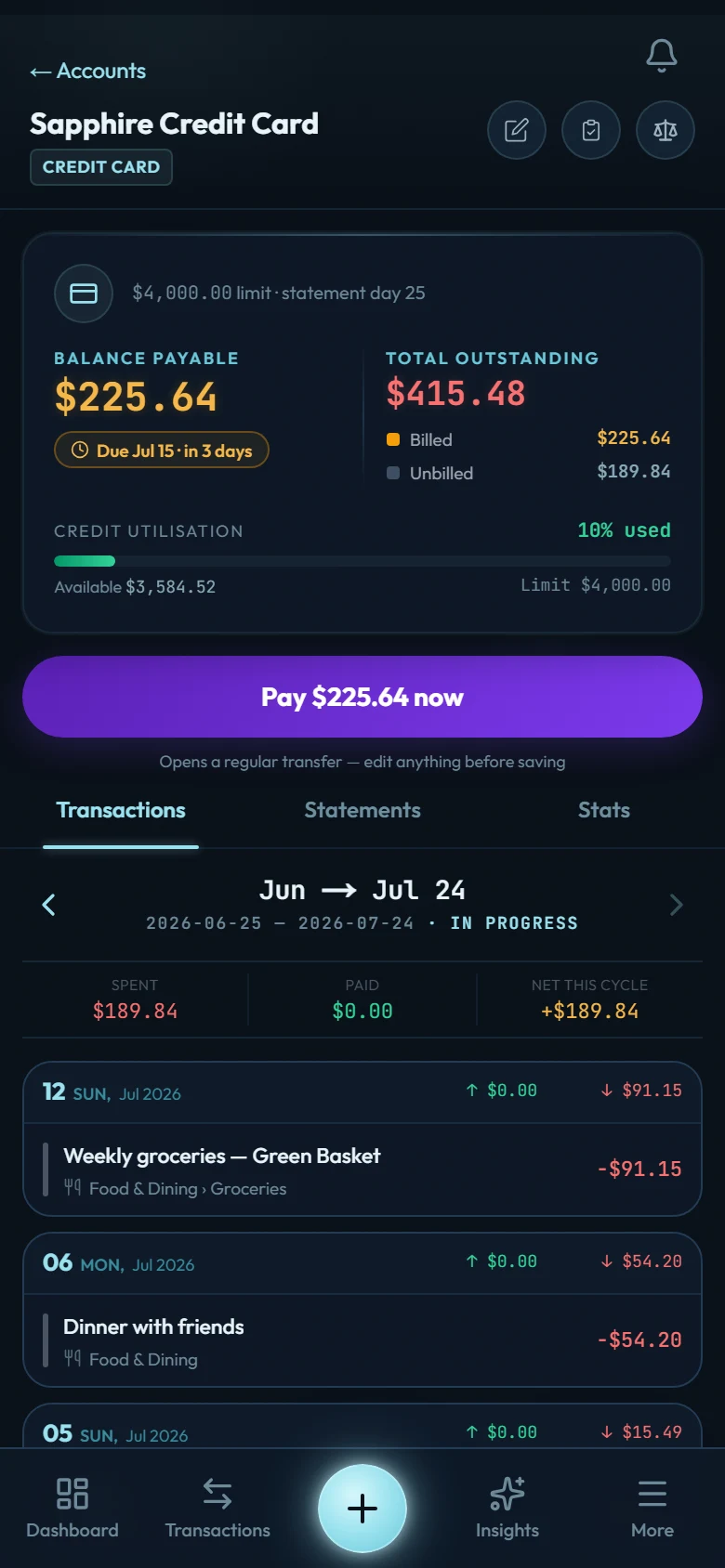

The cycle: current spend vs payable

The card's detail view separates two numbers people usually blur together:

- This cycle — what you've put on the card since the last statement closed. Not billed yet.

- Payable — everything that's been billed and not yet paid, across all closed statements — not just the most recent one. If an older bill is still partly unpaid, it stays in the payable until your transfers cover it. The due date shown is the oldest unpaid statement's due date, so a genuinely overdue bill surfaces instead of hiding behind a newer one.

When a statement closes, Wealth Mutant folds it into the payable and reminds you ahead of the due day (a Smart Insight carries the numbers; the push notification deliberately doesn't — amounts never appear in notification text). Payments apply oldest-bill-first, the way a bank clears arrears.

Paying the bill

Paying is a transfer from a bank account to the card — never an expense (the expenses were the purchases). Record it like any transfer; the card's owed amount falls accordingly. Partial payments are just smaller transfers.

Net worth

Card debt counts against you: net worth = what you own minus what you owe, cards and loans included. No hiding.